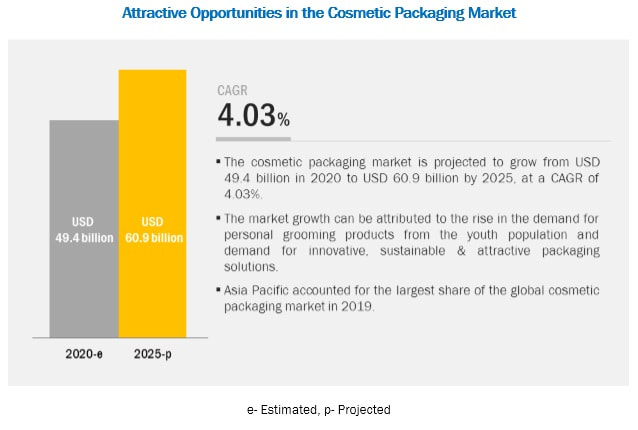

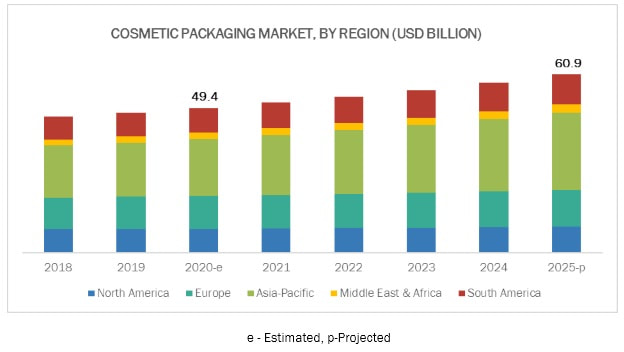

The global cosmetic packaging market size is projected to grow from USD 49.4 billion in 2020 to USD 60.9 billion by 2025, at a CAGR of 4.03% from 2020 to 2025. The market is projected to grow in accordance with the growth of the cosmetic industry across the globe. Factors such as an increase in the innovations in packaging, and a boost in the demand for cosmetics from the youth population is expected to drive the market for cosmetic packaging.

The Asia Pacific region accounted for the largest market share in 2019. The increase in demand in the region for cosmetic packaging can be largely attributed to the growing population, urbanization & disposable income of the population. Besides, there are less stringent norms and standards for the use of raw materials or ingredients for the manufacturing of packaging products, along with the easy availability of cheap labor, which is attracting the major players to expand their operations in the region. Furthermore, the increase in demand for cosmetics from the emerging economies of Asia Pacific is expected to boost the market for cosmetic packaging as well. To know about the assumptions considered for the study download the pdf brochure Key Market Players Key players, such as Amcor PLC (Australia), Berry Global Inc. (US), Sonoco (US), Albea SA (France), HCP Packaging (China), AptarGroup, Inc. (US), and Huhtamaki Oyj (Finland) have adopted these strategies to strengthen their product portfolios, expand their market presence, and enhance their growth prospects in the cosmetic packaging market. Amcor, formerly known as APM-Australian Paper Manufacturers, is a global packaging manufacturer that offers innovative packaging solutions to the customers. Amcor designs highly versatile packaging solutions which are innovative, available with a one-way integrated valve, and offer ease of disposal. Innovation, excellence in manufacturing, and a broad range of technologies are the key strengths of the company. The company is one of the key leaders in the cosmetic packaging market; faces strong competition from the global as well as the regional players. Recent Developments

0 Comments

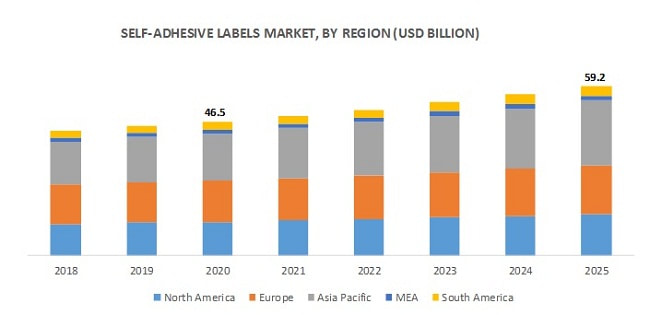

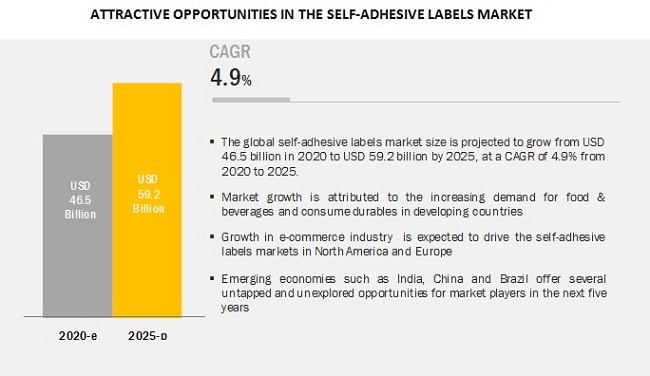

The global self-adhesive labels market size is projected to grow from USD 46.5 billion in 2020 to USD 59.2 billion by 2025, at a compound annual growth rate (CAGR) of 4.9% during the forecast year. The growth is attributed to the change in style of labeling, innovative & sustainable labeling solutions, increasing urban population leading to the increase in demand for home & personal care products, and boost in demand for packaged food and ready-to-eat meals, due to the rising working population.

The self-adhesive labels market is quite fragmented, but it has large players, such as Avery Dennison Corporation (US), CCL Industries Inc. (Canada), Sato Holdings Corporation (Japan), All4labels Group (Germany), Multi-Color Corporation (US), Coveris holdings Holdings S.A. (US), Fuji Seal International, INC. (Japan), Huhtamaki Oyj (Finland), LINTEC Corporation (Japan), Skanem S.A. (Norway), and Torraspapel Adestor (Spain). These players have adopted various growth strategies, such as expansions & investments, new product developments, mergers & acquisitions, to increase their market shares and enhance product portfolios. Mergers & acquisitions accounted for the largest share of all the strategic developments that took place in the self-adhesive labels market between 2016 and 2020. Key players such as Avery Dennison Corporation (US), CCL Industries Inc. (Canada), All4labels Group (Germany), Multi-Color Corporation (US), Coveris holdings Holdings S.A. (US), Fuji Seal International, INC. (Japan), Huhtamaki Oyj (Finland), LINTEC Corporation (Japan), Skanem S.A. (Norway) adopted these strategies to strengthen their business portfolios and presence in the self-adhesive labels industry. To know about the assumptions considered for the study download the pdf brochure CCL Industries Inc. is one of the leading label manufacturers and converters of pressure-sensitive and extruded film materials. Its customer base comprises global consumer products, healthcare, chemical, and durable goods companies. It operates through its four business segments: CCL (converter of pressure sensitive and specialty extruded film materials), Avery (supplier of labels, specialty converted media, and software solutions), Checkpoint Systems (developer of RF and RFID based technology systems), and Innovia (producer of specialty, high-performance, multi-layer, surface engineered films for label, packaging, and security applications). The company has a foothold and a strong customer base in Canada. It has corporate offices in Toronto, Ontario, Canada, and Framingham, Massachusetts, US. The company has its presence in about 42 countries, globally, and has a label and tube license holder operating two plants in Indonesia. Avery Dennison is one of the key players in the self-adhesive labels market and designs and produces a wide range of labelling and functional materials. The company’s product portfolio includes pressure-sensitive materials (for labels and graphic applications), tapes & other bonding solutions (for medical, industrial, and retail applications), tags, labels, and embellishments (for apparel), and radio-frequency identification (RFID) solutions (for retail apparel and other markets). It operates through three business segments: Label and Graphic Materials; Retail Branding and Information Solutions; and Industrial and Healthcare Materials. It offers self-adhesive labels through the Label and Graphic Materials segment. This business segment is responsible for the production of the pressure-sensitive labels and packaging materials & films for graphic and reflective products. Don’t miss out on business opportunities in Self-adhesive labels Market. Speak to our analyst and gain crucial industry insights that will help your business grow.  The global fresh food packaging market size is projected to grow from USD 79.8 billion in 2020 to USD 95.2 billion by 2025, at a CAGR of 3.5% between 2020 and 2025. The major driving factors of the market include growing demand for convenience food items and innovative packaging solutions for extended shelf life of fresh food items.

APAC is projected to be the fastest-growing market for fresh food packaging during the forecast period. Increase in demand for convenience by consumers and concerns about food product safety are some of the major reasons that could drive the fresh food packaging market in the region. However, the fresh food packaging market faces restraints such as stringent government rules and regulations regarding raw materials, which hinder the growth of the market. Download PDF Brochure to know more assumptions: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=240678791 The key players in the fresh food packaging market are Amcor PLC (Australia), Interntional Paper Company (US), WestRock Company (US), Sealed Air Corporation (US), Smurfit Kappa (Ireland), Coveris (Vienna), DuPont (US), DS Smith PLC (UK), Mondi PLC (South Africa), Silgan Holdings Inc. (US), Sonoco Products Co. (US), Schur Flexibles (Austria), Anchor Packaging Inc. (US), Printpack Inc. (US), Bomarko Inc. (US), Packaging Corporation of America (US), Graphic Packaging Holding Co. (US), Ampacet Corporation (US), Ultimate Packaging Limited (UK), and Temkin International Inc. (Utah). These players have adopted various strategies, such as merger & acquisition, investment & expansion, new product launch/development, and partnership, contracts & agreements, a joint venture between 2016 and 2020, to enhance their market shares and expand their global presence. Amcor PLC (Australia) is the largest player in the market. The company has its presence in North America, Europe, Asia Pacific, and in emerging markets. It is one of the leading companies engaged in the manufacturing and distribution of both plastic and fresh food packaging. The company focuses on increasing its profitability by strengthening customer relations and expanding its presence by adopting both inorganic and organic strategies, such as agreements and contracts in emerging markets while optimizing operational performance

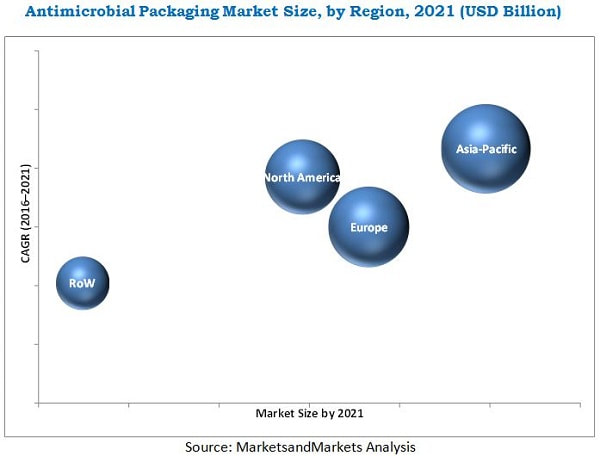

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=240678791 Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: [email protected] Visit Our Website: https://www.marketsandmarkets.com/  The antimicrobial packaging market size will grow from USD 7.28 Billion in 2015 to USD 10.00 Billion by 2021, at a CAGR of 5.54%. The demand in this market is supported by increasing demand in the Asia-Pacific region and wide application in diverse industries. Antimicrobial packaging is one of the forms of active and controlled-release packaging technologies. It helps to increase the shelf life of the product and prevents microbial contamination to the packed product while ensuring its safety and quality. Antimicrobial packaging is widely used in the food industry as a result of the rising consumer demand for products that are perishable, preservative-free, and minimally processed.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=84919936 Global antimicrobial packaging manufacturers and vendors are continuously adding innovation to their products & services to protect the enterprise networks against advanced persistent threats. Also, antimicrobial packaging solutions are being increasingly adopted in various verticals such as food & beverages, healthcare, consumer goods, personal care goods, and agricultural goods which have led to the growth of the market across the globe. Asia-Pacific is projected to have the largest market share during the forecast period with the highest potential for growth opportunities. The global market for antimicrobial packaging is dominated by players such as BASF SE (Germany), The Dow Chemical Company (U.S.), Mondi Plc (South Africa), PolyOne Corporation (U.S.), Biocote Limited (U.K.), Dunmore Corporation (U.S.), Linpac Senior Holdings (U.K.), Microban International (U.S.), Oplon Pure Sciences Ltd. (Israel), and Takex Labo Co. Ltd. These players have adopted various strategies to expand their global presence and increase their market share. New product developments, agreements, and acquisitions are some of the major strategies adopted by the market players to achieve growth in the market. The growth of the anti-microbial packaging market was largely influenced by new product development in the past 10 years. A large number of developments such as new product development, acquisitions, and agreements were made by top players in the market in 2015. New product development was the major strategy adopted by most of the players in the anti-microbial packaging market. Companies such as BASF SE, The Dow Chemical Company, and Mondi Group were the key players who adopted this strategy to increase the reach of their offerings and improve their production capacity. Also, the year 2015 saw a lot of acquisitions by key players to increase their geographic presence and expand their product portfolio to untapped markets. During this, Dow Microbial Control (U.S.), a business group of The Dow Chemical Company (NYSE: DOW), received approval from the United States Environmental Protection Agency for its innovative, solid form of KATHON Antimicrobial. KATHON 7 TL Antimicrobial solid tablets are packaged in a water-soluble film that dissolves rapidly with no residue, significantly reducing potential user contact with the active ingredients. Also, Dow Microbial Control (U.S.) and the manufacturer of SILVADUR Antimicrobial announced that Pulcra Chemicals (Germany) has been added to its global distributor network for SILVADUR Antimicrobial. Pulcra Chemicals is a leading global supplier of innovative specialty chemicals and systems solutions for increasing the productivity of manufacturing processes in the fiber, textile, and leather industries. Apart from this, Mondi Plc signed an agreement with Walki Oy (“Walki”) (Finland) for the acquisition of two extrusion coating plants located in Pietarsaari in Finland and Wroclaw in Poland. The acquisition would strengthen Mondi Plc’s position in the European extrusion coatings market and increase the range of technical capabilities offered to customers. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=84919936  The Industrial Labels market for industrial labels is projected to grow from USD 43.04 Billion in 2016 to reach USD 55.95 Billion by 2021, at a CAGR of 5.39%. The market for industrial labels is growing due to increasing demand in end-use industries such as construction, automotive, consumer durables, transportation & logistics, and aerospace & defense.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=177324755 Warning/security labels type gain maximum traction during the forecast period Warning/security labels type is highly preferred because of a variety of reasons such as to attract attention to warnings, to identify risks/hazards involved, to convey security messages, and to provide product-related information. These labels are highly used at the manufacturing sites such as automotive, construction, manufacturing, and marine to maintain a safe working environment. Transportation & logistics segment is projected to grow at the fastest rate during the forecast period The industrial labels market is segmented on the basis of end-use industry into transportation & logistics, construction, automotive, consumer durables, and others. In 2015, the transportation & logistics segment accounted for the largest share of the end-use industry segment and is projected to grow at the highest CAGR during the forecast period. The increasing e-commerce, online shopping businesses, increasing supply chain & warehousing industry, and governments’ initiatives to propel FDI have encouraged the industrial labels market to grow. Asia-Pacific to play a key role in the market for industrial labels On the basis of key regions, the market for industrial labels is segmented into North America, Europe, Asia-Pacific, and Rest of the World (RoW). The low labor costs, excellent industrialization, a huge scope for FDI, emerging economic conditions, stable government scenarios, and an excellent hold on industries such as construction, automotive, consumer durables, logistics, marine, and aerospace have played a crucial role in the growth of the market for industrial labels in the Asia-Pacific region. The key players considered in the report are:

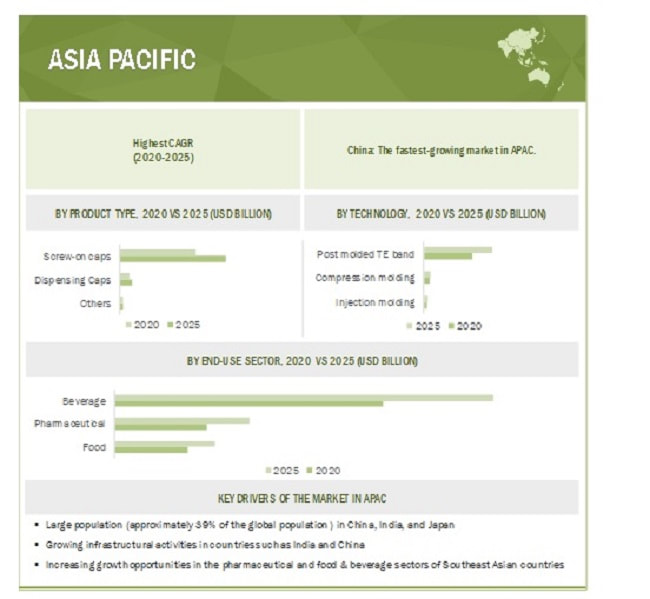

Developing countries such as China, India, and Brazil are poised to witness high demand for plastic caps & closures in the next few years. The growth is driven mainly by favorable demographics and a rise in household incomes. Convenience and hygiene are becoming highly valued attributes as packaged food products take up a growing share of the consumer’s expenditure due to changing lifestyles.

Other emerging economies, such as Mexico, Turkey, South Africa, and Indonesia, are promising markets for plastic caps & closures owing to the growth of the FMCG sector in these countries. Cap manufacturers are adopting aggressive growth strategies in these countries by diversifying their product offerings and strengthening their distribution base. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=132939537 Increase in demand for bottled water, need for convenience, concerns about product safety & security, product differentiation & branding, and decreasing package sizes are driving the market for plastic caps & closures. The global plastic caps and closures market size is projected to grow from USD 44.3 billion in 2020 to USD 57.0 billion by 2025, at a CAGR of 5.2% between 2020 and 2025. A plastic cap plays a key role in safeguarding the product from dust and other microbes. Plastic caps & closures are cost-effective as compared to metal caps & closures. Consumers are on the lookout for closures that are user-friendly, easy to open, and convenient to use. The rising popularity of dispensing closures and pump closures in various product groups such as body care, skincare, beverages, and liquid food products is likely to spur the growth of the plastic caps & closures market, globally. The health and wellness trend is now shifting toward preventive healthcare, propelling the demand for FMCG products that target improved lifestyles. Plastic caps & closures that prevent contamination, tampering, and counterfeiting are becoming increasingly important to reassure consumers about the safety and authenticity of the products that they are buying. The pharmaceutical industry is projected to register the highest growth It is very important to maintain the quality of pharmaceutical products during the manufacturing process. Pharmaceutical products can be contaminated through air particles, dust, and microorganisms. To avoid contamination, plastic caps & closures are used to seal the medicines in the pharmaceutical industry. The packaging of healthcare products is of utmost importance to protect the contents from air, dust, and moisture. An increase in chronic ailments, an increase in the aging population, and a rise in disposable income in developing nations drive the demand for healthcare products, thereby driving the demand for plastic caps & closures. North America is projected to be the fastest-growing market for plastic caps & closures during the forecast period. The increase in consumption of CSDs and packaged food, high disposable income levels, and growth in demand for convenience food are supporting the market in North America. Improvements in the economic situation and rise in demand for innovative packaging also contribute to the growth of the plastic caps & closures market. The growth in this region, especially in the US, has been exponential over the last five years. Plastic closures have been replacing every possible type of closures in North America. Inquire before buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=132939537  The blister packaging market size is projected to grow from USD 24.1 billion in 2020 to USD 34.1 billion by 2025, at a CAGR of 7.2%. The blister packaging market is witnessing growing demand from end-use industries such as healthcare, food, consumer goods, and industrial goods. Its growth is attributed to cost-effectiveness and tamper-evident design for product protection.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=24775059 Emerging economies such as BRIC (Brazil, Russia, India, and China) and CIVETS (Colombia, Indonesia, Vietnam, Egypt, Turkey, and South Africa) are poised to account for much of the global growth for blister packaging in the upcoming years. Growth in these countries is mainly driven by the favorable demographics, rising household incomes, and changing lifestyles of consumers, encouraging a rising preference for on-the-go products. These factors induce changes in lifestyle that lead to greater demand for convenience in terms of packaging and use. There has been a gradual shift in consumer choice from traditional bottles for pharmaceutical products to blister packaging, which is unit-dose packaging. Blister packs are used in the healthcare industry for drugs and medical devices. They are also used in wide applications in consumer goods, industrial goods, and food industries. Moreover, blister packaging requires fewer resources for packaging, occupy less retail shelf space, and offer an excellent hang-hook display. Hence, blister packs are available at a lower cost as compared to other packaging formats, such as rigid bottles, making them cost-effective. Recent Developments

The key players in the blister packaging market are as Amcor Plc (Switzerland), DOW (US), WestRock Company (US), Sonoco Products Company (US), Constantia Flexibles (Austria), Klockner Pentaplast Group (Germany), E.I. du Pont de Nemours and Company (US), Honeywell International Inc. (US), Tekni-Plex (US), Display Pack (US). The blister packaging market report analyzes the key growth strategies adopted by the leading market players, between 2015 and 2020, which include expansions, merger & acquisition, new product developments, and collaborations. Speak with Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=24775059  The global cosmetic packaging market size is projected to grow from USD 49.4 billion in 2020 to USD 60.9 billion by 2025, at a CAGR of 4.03% from 2020 to 2025. The market is projected to grow in accordance with the growth of the cosmetic industry across the globe. Factors such as an increase in the innovations in packaging, and a boost in the demand for cosmetics from the youth population is expected to drive the market for cosmetic packaging.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1307 In terms of value and volume, bottles are estimated to lead the cosmetic packaging market Bottles, by type, accounted for the largest market share among all the types of cosmetic packaging because of the increase in demand for bottles from the personal care and hair care manufacturers. Bottles can be customized according to the requirements of the customers and maybe printed with unique ideas & patterns. The bottles are an ideal choice for most of the cosmetic products such as lotions, body wash, shampoos, conditioners, and many more. In terms of value and volume, rigid plastic is estimated to lead the cosmetic packaging market The rigid plastic, by material, led the cosmetic packaging market in 2019, in terms of value and volume. Rigid plastic packaging involves the use of plastic materials; this form of packaging has an inflexible shape or form. Factors such as being lightweight and a cost-effective packaging solution for cosmetic products will boost the demand of rigid plastic bottles, jars, and containers for the cosmetic packaging industry (specifically for the color cosmetics, skin care and hair care application). Skin care is estimated to be the largest segment in the cosmetic packaging market Skin care, by application, accounted for the largest demand for cosmetic packaging in 2019, in terms of value and volume. This dominant market position is attributed to the boost in the demand for new and innovative skin care ranges such as face creams, anti-aging creams, sunscreens, and others. With the boost in the demand for personal grooming products, the demand for its packaging product has also gone up, which has created an opportunity for the growth of the skin care segment in the cosmetic packaging market. The Asia Pacific region is projected to account for the largest share in the cosmetic packaging market The Asia Pacific region is projected to lead the cosmetic packaging market, in terms of both value and volume from 2020 to 2025. An Increase in demand for cosmetic products in emerging economies, as well as a boost in consumer awareness drives the investments of manufacturers to develop unique & innovative packaging solutions. This, in turn, increases the demand for cosmetic products, and is further expected to boost the demand for packaging in the Asia Pacific region. Amcor PLC (Australia), Berry Global Inc. (US), Sonoco (US), Huhtamaki Oyj (Finland), Albea SA (France), and DS Smith PLC (UK) are the key players operating in the cosmetic packaging market. Expansions, acquisitions, and new product developments are some of the major strategies adopted by these key players to enhance their positions in the cosmetic packaging market. Inquiry before buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=1307 Growth of the food & beverages industry is expected to drive the market for self-adhesive labels2/25/2021  The global self-adhesive labels market size is projected to grow from USD 46.5 billion in 2020 to USD 59.2 billion by 2025, at a CAGR of 4.9%. The demand for self-adhesive labels can be attributed to the increasing disposable incomes of people in developing countries and changing preferences of manufacturers for cost-efficient and effective labeling, which compel people to rely on modern labeling techniques. Lack of awareness about various types of labeling techniques factors in decreasing the demand for labels. Varying environmental mandates in terms of printing on labels across different regions and the increasing cost of raw materials are significant challenges faced by manufacturers.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=96664367 A large number of self-adhesive labels are used in the food industry for fresh food, meat, fish, seafood, fresh produce, poultry, and ready meals. Increase in demand for convenience and quality food products has led the market for self-adhesive labels. Recent Developments In March 2020, CCL Industries Inc. acquired Flexpol sp. z.o.o. (Flexpol), which currently trades as Innovia Poland. This acquisition is expected to enhance the existing capabilities of the company to serve the label industry in the European region. In March 2020, Coveris acquired Plasztik-Tranzit Kft (Hungary), a producer of flexible packaging solutions for the food industry. The acquired company is renamed as Coveris Pirto and is a part of Coveria Holdings. This strategic development is expected to create a center for high-tech packaging manufacturing in East Europe and to boost the production capability of the company in the medical, food, and films end-markets. The APAC region is projected to lead the self-adhesive labels market, in terms of both value and volume from 2020 to 2025. The usage of self-adhesive labels in the region has increased due to cost effectiveness, easy availability of raw materials, and demand for product labeling from highly populated countries such as India and China. The increasing scope of applications of self-adhesive labels in the food & beverage, healthcare, and personal care industries in the region is expected to drive the self-adhesive labels market in APAC. The growing population in these countries presents a huge customer base for FMCG products and food & beverages. Industrialization, growing middle-class population, rising disposable income, changing lifestyles, and rising consumption of packed products are expected to drive the demand for self-adhesive labels during the forecast period. Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=96664367 The global plastic caps and closures market size is projected to grow from USD 44.3 billion in 2020 to USD 57.0 billion by 2025, at a CAGR of 5.2% between 2020 and 2025. Factors such as the need for convenience and better operability act as important drivers for plastic caps & closures. A plastic cap plays a key role in safeguarding the product from dust and other microbes. Plastic caps & closures are cost-effective as compared to metal caps & closures. Consumers are on the lookout for closures that are user-friendly, easy to open, and convenient to use. The rising popularity of dispensing closures and pump closures in various product groups such as body care, skincare, beverages, and liquid food products is likely to spur the growth of the plastic caps & closures market, globally. The health and wellness trend is now shifting toward preventive healthcare, propelling the demand for FMCG products that target improved lifestyles. Plastic caps & closures that prevent contamination, tampering, and counterfeiting are becoming increasingly important to reassure consumers about the safety and authenticity of the products that they are buying. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=132939537 Recent Developments In July 2019, Berry Global Group acquired RPC Group for approximately USD 6.5 billion. This acquisition helped create a leading global supplier of value-added protective solutions and one of the world’s largest plastic packaging companies. Also, the company has broadened its global footprint consisting of over 290 locations worldwide, including in North and South America, Europe, Asia, Africa, and Australia. In June 2019, Amcor acquired Bemis Company Inc. The combined company will now operate as Amcor Plc (Amcor). The acquisition of Bemis has brought additional scale, capabilities, and footprint that has strengthened Amcor’s industry-leading value proposition and generate significant value for shareholders. North America is projected to be the fastest-growing market for plastic caps & closures during the forecast period. The increase in consumption of CSDs and packaged food, high disposable income levels, and growth in demand for convenience food are supporting the market in North America. Improvements in the economic situation and rise in demand for innovative packaging also contribute to the growth of the plastic caps & closures market. The growth in this region, especially in the US, has been exponential over the last five years. Plastic closures have been replacing every possible type of closures in North America. Berry Group (US), Crown Holding (US), AptarGroup (US), Amcor (Australia), BERICAP (Germany), Coral Products (UK), Silgan Holdings (US), O.Berk Company, LLC (US), Guala Closures (Italy), United Caps (Luxembourg), Caps & Closures Pty Ltd. (Australia), Caprite Australia Pty Ltd. (Australia), Pano Cap (Canada) Limited (Canada), Plastic Closures Ltd. (UK), Cap & Seal Pvt. Ltd. (India), Phoenix Closures (US), Alupac India (India), Hicap Closures (China), MJS Packaging (US), J.L. Clark (US), TriMas (US), and Comar, LLC (US) are some of the players operating in the global plastic caps & closures market. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

December 2021

Categories |

RSS Feed

RSS Feed